This week, the iGaming stock market in general consists mainly of positive momentum from the majority of mid-cap and larger-cap operators, with only some small caps providing adverse price performance. Throughout the iGaming portion of the economy, we have also seen a continued shift from the formerly aggressive growth stage toward a more sustainable level of profitability or efficiency, especially in regard to the U.S marketplace.

Moreover, external pressures arising from both new prediction markets and uncertainty in other international regulations will continue to impact investor feelings about the and thus create volatility even though the current operating statistics of the iGaming space has proven to be healthy.

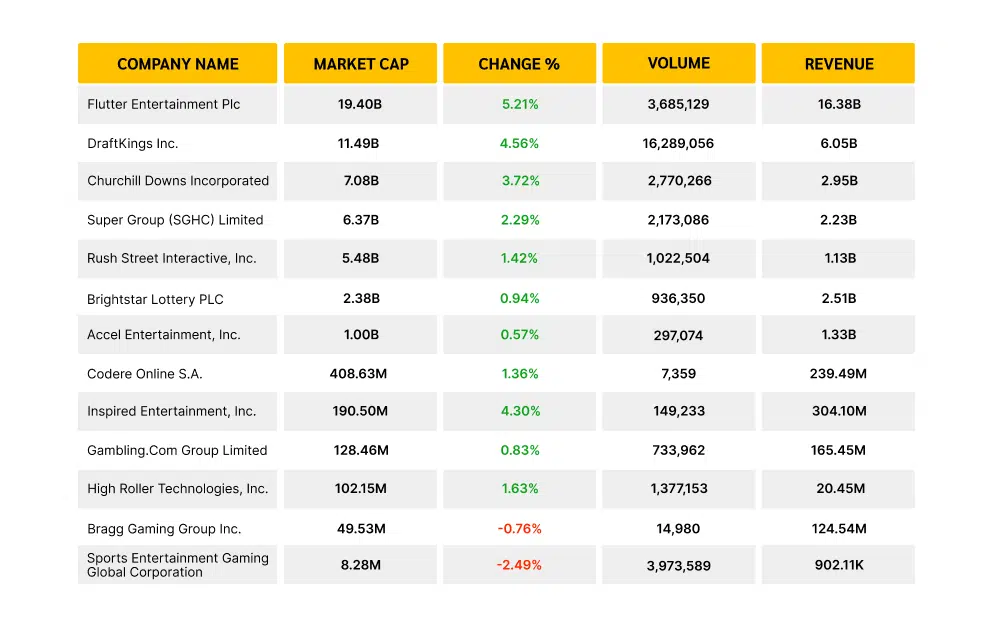

Market Overview

Top Performers (Growth Leaders)

Flutter Entertainment Plc (+5.21%)

- Remains the largest company in the segment (~$19.4B market cap).

- Strong revenue base ($16.38B) and dominant U.S. position via FanDuel.

- Growth supported by product innovation and high engagement levels.

DraftKings Inc. (+4.56%)

- Continues to show high trading volume (16.2M) – strongest investor activity in the dataset.

- Market narrative: shifting toward profitability after aggressive expansion.

- Strong engagement metrics and improving margins support bullish sentiment.

Inspired Entertainment (+4.30%)

- Outperforming relative to size, suggesting renewed investor interest in smaller tech-driven suppliers.

Two of the most prominent and highly regarded sports betting companies in the market today include both Flutter Entertainment Plc. and DraftKings Inc. Together, they make up a huge percentage of total market shares and continue to be leading indicators of overall market activity due to their dominance in both Europe and the U.S., respectively. Both companies continue to dominate the market but have different business models and value propositions. For example, Flutter has recently seen tremendous growth as a result of being an enormous, diversified, and global operation with a strong presence in both Europe and North America, which has enabled them to capitalize on this market opportunity.

While DraftKings is also a major player, they have been much slower to gain traction in both of these markets due to their focus on becoming profitable and their lack of marketing presence in both of these markets prior to the pandemic. Smaller-scale but more rapidly growing companies, such as Inspired Entertainment, have also benefited from the renewed focus placed on niche technology-based gaming companies. Thus, the overall trend in this segment is that investors prefer to invest in well-established companies with proven growth potential and strong brand ecosystems.

Mid-Tier Stability (Consistent Performers)

Churchill Downs Incorporated (+3.72%)

- Benefits from a diversified business model combining racing, gaming, and digital wagering.

- Supported by stable cash flows from established U.S. operations and strong seasonal event performance.

- Growth reflects steady investor confidence in hybrid land-based and online exposure.

Super Group (SGHC) Limited (+2.29%)

- Maintains consistent performance driven by its global online sportsbook and casino brands.

- Revenue base supported by strong international reach and scalable digital operations.

- Market positioning reflects steady growth in emerging and regulated markets.

Rush Street Interactive, Inc. (+1.42%)

- Shows stable upward movement with a focus on U.S.-centric online casino and sportsbook growth.

- Improving user engagement and retention metrics support long-term profitability outlook.

- Performance reflects gradual scaling rather than aggressive expansion.

The mid-tier has a more even and stable performance because the companies (e.g., Churchill Downs, Super Group, and Rush Street Interactive) have consistently reported smaller incremental increases. The mid-tier operators benefit from a diversified business model that includes a combination of online gaming, retail and hybrid product offerings, which helps mitigate the potential for high volatility compared to pure-play digital operators.

There is a consistent level of investor confidence in the mid-tier because the mid-tier operators are considered dependable contributors to the overall growth of the industry rather than being perceived as having a high-risk-high-reward-quick-return profile. In addition to not experiencing the same explosive capital inflows as the more prominent operators, their gradual upward price movements demonstrate continued confidence in their ability to generate sustainable revenues and consistently execute on their operational plans.